What Salary Do You Need To Live In London In 2026?

What salary do you need to live in London? Compare flatshare vs solo renting, take-home pay, borough rents, and family costs using 2026 data.

Author:James RowleyApr 04, 2026314 Shares62.8K Views

Salary You Need To Live In London As A Flatsharer, Solo Renter, Or Family

A realistic Londonsalary depends first on whether you flatshare, rent alone, or support children, because housing and childcare change the answer more than almost anything else.

In Short

- For a single person in a flatshare, London often starts to feel workable at around £35k to £45k

- For a single person renting alone, a more realistic range is often £55k to £70k+

- For many singles, £50k to £60kis where London starts to feel more comfortable

- For families, the answer rises fast because housing and childcarechange the maths

- Take-home pay matters more than headline salary

- Inner London usually needs more income than Outer London

| Living setup | What your salary needs to cover |

| Flatshare | Essentials, commute, some savings, and a modest social life |

| Rent alone | Much higher housing cost and much less room for error |

| Couple | Shared fixed costs help, but rent still dominates |

| Family | Housing and childcare become the biggest pressure points |

If you are comparing a London job offer with your current life elsewhere, the usual mistake is simple: people look at the salary first and the living setup second. It helps to understand the wider cost of living in londonfirst, but in practice rent is still the factor that changes the answer most. In practice, London works the other way round.

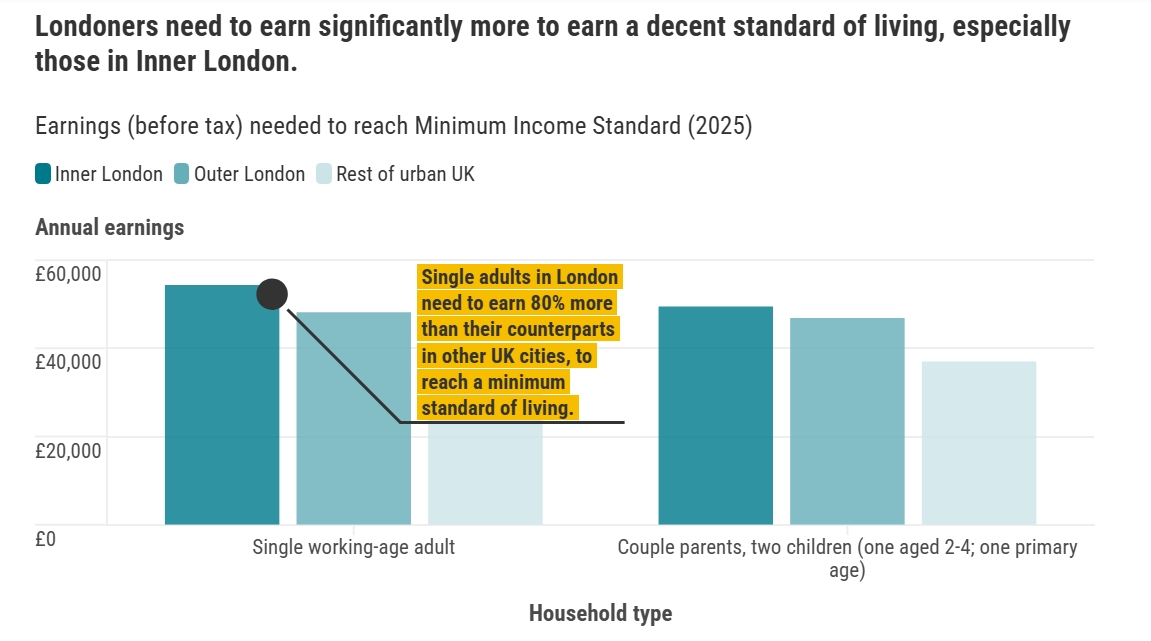

Trust for London’s latest Minimum Income Standard research says a single adult in Inner London needs £54.4k a yearfor a decent standard of living, while the ONS says average private rent in London was £2,273 a monthin February 2026.

That is before council tax, transport, food, or savings. Data as of March 2026 for the MIS figure and February 2026 for rent.

Quick Answer By London Living Setup

This section gives you the quickest honest answer. These are not legal thresholds or guaranteed outcomes. They are practical salary bands based on current London rents, take-home pay rules, and London-specific living-standard research.

What A Workable Salary Looks Like In A Flatshare

For many single adults, around £35k to £45kis where London starts to look workable in a flatshare rather than constantly fragile. That usually means you can cover a room, bills, transport, food, and still leave a little margin, but you are not living lavishly.

London room rents averaged £985 a month including billsin Q4 2025 on SpareRoom’s index, while London median gross weekly pay by residence was £902.70in 2025. Data as of January 2026 for room rents and 2025 for earnings.

What A Workable Salary Looks Like If You Rent Alone

If you want to rent alone, the answer shifts sharply. For many singles, £55k to £70k+is the more realistic starting point for a one-bed lifestyle that does not feel permanently exposed. That is not because London salaries are low. It is because solo housing swallows such a large share of your net pay.

Trust for London’s latest MIS already puts a single adult in Inner London at £54.4kfor a decent standard of living, and average private rent across Londonis £2,273 a month.

What Changes For Couples

Couples benefit from shared fixed costs, so a combined income can go further than two separate single budgets. In practice, a couple can often make London work on less than two solo-renter salaries, but only if rent, commute patterns, and savings expectations are sensible. The point is not that London becomes cheap. The point is that one rent split two ways changes the whole equation.

What Changes For Families

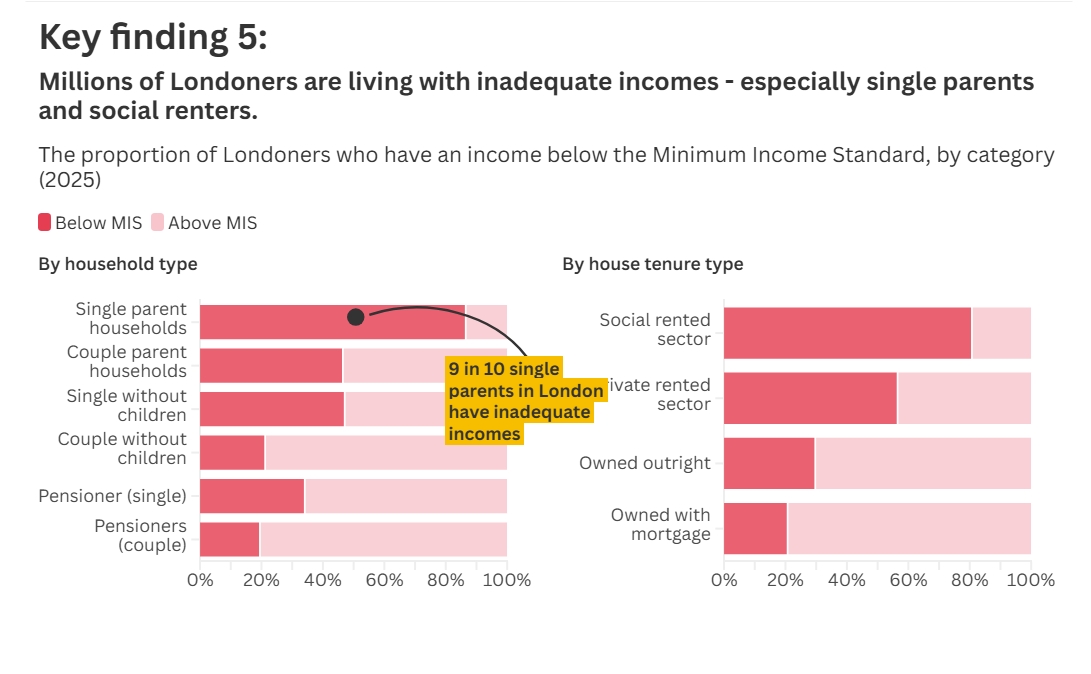

Families are where tidy salary answers break down fastest. The big multiplier is not just a larger home. It is childcare. Trust for London says the main drivers of London’s extra cost versus the rest of urban UK are rent and childcare, and 86.5% of single-parent householdsfall below the minimum income threshold. Data as of March 2026.

Quick view

| Setup | Broad salary read |

| Single in a flatshare | Often workable from about £35k to £45k |

| Single renting alone | More realistic from about £55k to £70k+ |

| Couple without children | Can work on less than two solo-renter salaries because fixed costs are shared |

| Family with children | Needs a much higher threshold because childcare and larger housing change the maths |

The important point is simple: flatshare, rent-alone, couple, and family budgets are not the same question, so they should never get the same answer.

Why The Number Changes So Much In London

Housing Is The Main Reason

Housing is the first thing I would check on any London salary. The ONS says average private rent in London was £2,273 a monthin February 2026, the highest of any English region.

SpareRoom’s room-rent data paints a very different picture for sharers, with a London average of £985 a month including billsin Q4 2025. Those are not small differences. They are the reason one person says £40k is fine and another says £40k is impossible.

Inner London And Outer London Are Not The Same

London is not one market. Trust for London says the gap is largest for single working-age adults, who need 78% more in Inner London than in the rest of urban UK, and 58% more in Outer London.

That becomes much easier to see when you look at the average rent in london by borough, because the same salary can feel manageable in one area and stretched in another.

Borough-level rent differences matter. A salary that feels workable in one Outer London borough can feel strained in a higher-rent Inner London borough, even before council tax, transport, and utilities are added.

Children And Childcare Change The Maths Fast

A child does not just add another food budget. It can mean bigger housing, childcare, school travel, and a lot less slack when something unexpected lands. That is why broad single-person salary advice becomes weak the moment a household includes children. Trust for London makes the same point clearly: rent and childcare are the main extra costs.

Take-home Pay Matters More Than Headline Salary

A £50k offer sounds strong until you map it to actual monthly money. For the 2026 to 2027 tax year in England, the personal allowance is £12,570, the basic tax rate is 20%up to £37,700above that, and employee Class 1 National Insurance is 8%to the upper earnings limit, then 2%above it.

That means London affordability is really a net-pay problem, not just a gross-salary problem. Data as of April 2026.

Once you see those four levers clearly, the salary bands stop looking random and start looking like simple consequences of rent, childcare, and tax.

The Benchmarks That Actually Matter

The useful move is to compare your income with the few benchmarks that genuinely tell you something.

Minimum Income Standard For London

The strongest benchmark in this topic is the Minimum Income Standard for London. Trust for London’s2025 update says a single adult in Inner London needs £54.4ka year for a decent standard of living, compared with £30.5kfor the equivalent in the rest of urban UK.

It also says almost half of Londonersdo not earn enough to reach the threshold. That tells you two things at once: London’s cost problem is real, and a “good salary” is not the same thing as the legal minimum. Data as of March 2026.

London Living Wage Versus National Living Wage

The London Living Wageis currently £14.80 an hour, while the statutory National Living Wageis £12.71 an hourfrom 1 April 2026 for workers aged 21 and over. Both matter, but they answer different questions.

The London Living Wage is a voluntary cost-of-living benchmark. The National Living Wage is the legal floor. Neither should be mistaken for “the salary you need to live comfortably in London.” Data as of April 2026.

UK Average Salary Versus London Pay

National context helps, but only briefly. ONS says median gross annual earnings for UK full-time employees were £39,039in April 2025. Nomis shows London median gross weekly pay at £902.70 by residenceand £958.20 by workplacein 2025, which is why London salaries often look higher on paper.

The catch is obvious once you pair that with London rent levels: higher pay does not automatically buy an easier life.

What Salary Feels Tight, Workable, Comfortable, And Strong In London

Here is the blunt version, based on current rent levels, London earnings, and the London MIS benchmark.

| Salary band | What it usually feels like in London |

| Under £35k | Tight. Usually shared housing and little room for savings |

| £35k to £45k | Workable for many flatsharers, but still trade-offs |

| £50k to £60k | More comfortable for many singles, especially with sensible rent |

| £60k+ | Stronger position. Solo renting becomes more realistic |

| £80k+ | Much more choice, though London can still absorb a lot |

These bands are judgement calls, but they are grounded in current London rent levels, London-specific living-standard research, and 2026 to 2027 take-home pay rules.

Tight But Possible

Under about £35kis usually survival-with-compromise territory for a single adult in London. That often means a flatshare, careful spending, limited savings, and not much room for rent shocks or lifestyle creep. Once you add a long commute, student loan, or pension contribution, it tightens fast.

Workable With Trade-offs

Around £35k to £45kis where London becomes more workable for many singles in shared housing. You can usually cover the basics without feeling that one bad month will undo everything, but the trade-offs are still real. You are not choosing freely between central solo renting and strong monthly saving.

Comfortable For A Single Person

For many single people, £50k to £60kis where London starts to feel more comfortable, especially if you are not insisting on a solo one-bed in a pricier Inner London area.

At that level, take-home pay is materially stronger, and you have a better chance of covering essentials, saving, and still having some normal city life. That sits far closer to Trust for London’s single-adult MIS benchmark than the lower salary bands do.

Strong Enough To Rent Alone More Safely

£60k and aboveis where solo renting starts to look more plausible without immediately leaning on luck, debt, or a tiny emergency buffer. Even then, borough choice matters.

If you want a nicer one-bed, a short commute, and real monthly savings, you can still feel squeezed. London is perfectly capable of making a decent salary feel ordinary.

Why The Same Salary Can Feel Very Different In Practice

Two people on £50k can be living completely different versions of London. One is flatsharing in Zone 3 with low commute costs. The other is solo renting with expensive travel and higher bills. Same salary, different city. That is why the better question is not “Is £50k good?” It is “What does £50k need to pay for?”

That judgement leads neatly into the next section, because salary only becomes real once you convert it into monthly money.

What Different Salary Levels Really Feel Like In London

The figures below are rough PAYE estimates for England using 2026 to 2027 income-tax and employee National Insurance thresholds, with no student loan and no pension deduction. They are useful planning figures, not personal tax advice. Data as of April 2026.

| Salary | Approximate monthly take-home |

| £30k | £2,093 |

| £40k | £2,693 |

| £50k | £3,293 |

| £60k | £3,780 |

| £80k | £4,746 |

£30k

At £30k, monthly take-home is roughly £2,093. For London, that usually means a flatshare and close attention to spending. Renting alone is not a realistic default.

£40k

At £40k, monthly take-home is roughly £2,693. This is much more workable for a shared-house life, especially outside the most expensive pockets, but it is still not a comfortable solo-renter salary in much of London.

£50k

At £50k, monthly take-home is roughly £3,293. This is the point where many single workers feel London starts to become manageable rather than purely defensive, especially if they share housing or live farther out.

£60k

At £60k, monthly take-home is roughly £3,780. This is a noticeably stronger position, and for many singles it is where solo renting becomes more plausible, though not automatically comfortable everywhere.

£80k And Above

At £80k, monthly take-home is roughly £4,746. That gives you far more choice, but London can still burn through it quickly if you want a better one-bed, short commute, frequent eating out, and aggressive saving at the same time.

Rent-burden stress test

This table makes the solo-renting problem much clearer. It compares the ONS average London private rent of £2,273 a month with the take-home pay figures above. It is not a personal affordability rule, but it shows how quickly average solo rent can dominate a London budget.

| Salary / Approx monthly take-home | Average London rent as a share of take-home |

| £30k / £2,093 | 109% |

| £40k / £2,693 | 84% |

| £50k / £3,293 | 69% |

| £60k / £3,780 | 60% |

| £80k / £4,746 | 48% |

A salary can sound decent until you test it against average solo rent. Once you do that, flatsharing and renting alone stop looking like small lifestyle differences and start looking like completely different affordability questions.

Monthly Budget Examples That Make The Answer Easier To Judge

This section turns the salary bands into lived budgets. These are not universal budgets. They are realistic examples to help you judge what sort of income actually matches your target lifestyle.

Single Person In A Flatshare

A typical flatshare budget might look something like this:

- Room rent including bills: about £985

- Transport: £150 to £220

- Groceries and basics: £250 to £320

- Phone, subscriptions, and small fixed costs: £50 to £100

- Social life and miscellaneous spending: £200 to £350

- Savings buffer: £100 to £250

That is why a salary in the high £30k to low £40k range often feels workable rather than generous.

Single Person Renting A One-bed Alone

For a solo renter, the same exercise changes fast:

- Average private rent in London: £2,273

- Council tax and utilities: often several hundred pounds more

- Transport: £150 to £220

- Groceries and basics: £250 to £320

- Savings buffer: whatever is left after housing stops dominating the month

This is the cleanest reason many London salary discussions go wrong. They quietly compare a flatshare salary with a rent-alone lifestyle.

Couple Without Children

A couple without children can spread rent, bills, and internet across two incomes. That usually makes a combined income go further than two single budgets. But if the couple wants a one-bed or two-bed in a more expensive borough, the benefit of splitting costs can disappear surprisingly quickly. The deciding factor is still housing.

Family With Childcare

Trust for London’s research says rent and childcare are the biggest extra costs in the capital, and that is exactly what most family budgets feel like in practice. Once nursery fees or wraparound care enters the picture, a salary that looked decent for a couple can stop feeling decent very quickly.

Worked Family Example

A child-free couple on a combined income that feels workable in London can still see the budget tighten sharply once one child and regular childcare are added. The income has not changed, but the household may now need more space, higher travel coordination, and childcare costs that can erase much of the spare monthly margin.

That is exactly why family salary advice should be treated separately from single-person or couple-without-children advice.

Rent

Rent is the first filter. If your target lifestyle requires a property type or borough you cannot comfortably cover, the rest of the budget is just damage control.

Council Tax And Utilities

These are rarely the headline cost, but they are the reason “the rent looks okay” can turn into “the month feels tight”. This is especially true for solo renters who have nobody to split fixed household costs with.

Transport

Transport matters more than many salary breakdowns admit. A cheaper rent farther out can still be worth it, but only if the commute cost and time do not cancel out the saving.

Food And Essentials

Food is not the main London problem. Housing is. But once rent is heavy, normal food spending becomes the part people feel guilty about, even when the real issue is that the housing setup was too expensive to start with.

Savings Buffer

A London salary does not feel comfortable until it can absorb ordinary shocks. If there is no room for savings, the budget may be livable on paper and still not be secure in practice.

Editor’s Take

My rule is simple: if a London salary works only before bills, or only if nothing goes wrong, it is not really enough.

Those monthly examples lead to the most common trap of all, which is treating solo renting like the default.

Renting Alone In London Is A Separate Question

People often ask if a salary is enough for London when what they really mean is: is it enough to rent alone in London.

Why One-bed Rent Changes Everything

Once you move from a room to a whole flat, the whole budget tilts. You are not just paying more rent. You are taking on council tax, full utility bills, and every household fixed cost by yourself. That is why the jump from flatsharing to renting alone is much bigger than the jump from £30k to £40k.

Using The 30% Rent Rule Carefully

The 30% rule is useful as a warning light, not a universal law. If your rent is swallowing far more than about a third of your income, you are more likely to feel squeezed. In London, many people stretch past that anyway, but that does not mean it is comfortable. It usually means housing has become a trade-off against savings, space, or sanity.

When Flatsharing Is The More Honest Default

A lot of London job offers make far more sense when you treat flatsharing as the real starting point. That is not failure. It is the city’s housing maths. If your priority is getting to London, building savings, or testing an area before you commit, a flatshare can be the financially sane answer.

The honest takeaway is that “enough for London” and “enough to rent alone in London” are often very different salary thresholds.

What Is A Good Salary In London For A Family

Families need a more cautious answer because the costs are less forgiving. If you are planning around children, the number has to work under more pressure, not just in a good month.

Couple Without Children

A child-free couple can often make London work on a combined income that would feel weak for two separate solo-renter budgets. Shared rent and shared bills help. But the benefit is only real if the home size and location stay sensible.

One Child And Childcare

This is where London gets serious. Trust for London highlights childcare as one of the main reasons the capital costs so much more than the rest of urban UK. For a family, the salary question stops being “Can we cover the bills?” and becomes “Can we cover the bills andstill absorb childcare without wiping out savings?”

Why Family Costs Rise Faster Than People Expect

Families do not just scale up neatly. A second bedroom, childcare, school logistics, and less flexibility on where to live all push in the same direction. That is why any breakdown that gives one family salary number without asking about housing and childcare is oversimplifying the problem.

Local Reality Check

If I were judging a London family budget, I would look at childcare before holidays, eating out, or almost any other lifestyle line. It is one of the few costs big enough to change the whole answer.

That brings us to the most practical section of the page: how to judge a real offer.

Before You Accept A London Job Offer

This section is about decision-making, not theory. If you are moving for work, these are the checks that stop a decent-looking offer becoming an expensive mistake.

Check The Take-home Pay, Not Just The Salary

Use net pay as your real starting point. Gross pay is for comparison. Monthly take-home pay is what actually pays London rent.

Check The Commute Cost And Time

A cheaper area can be smart, but not if the commute eats back the saving or damages your week enough that you end up spending more elsewhere.

Check Whether The Job Assumes Hybrid Or Office-heavy Working

Three office days and five office days are different budgets. They are also different transport costs, meal costs, and time costs.

Check Whether The Salary Still Works If Rent Rises

London housing rarely rewards fragile planning. If the budget only works at today’s rent and with no buffer, it is not a stable London budget.

Check Whether You Can Still Save Something Each Month

This is the simplest stress test of all. If the answer is no, the salary may be livable, but it is not yet strong.

Quick checklist

- Work out your likely monthly take-home pay.

- Decide whether you are flatsharing or renting alone.

- Price the commute honestly.

- Add a realistic savings buffer.

- Ask whether the plan still works if rent goes up.

If you can answer those five checks clearly, you usually no longer need a vague internet answer. You know whether the salary works for yourLondon.

Frequently Asked Questions

Is £30k Enough In London?

Usually only with shared housing and a careful budget. At roughly £2,093 a month take-homeunder standard 2026 to 2027 PAYE assumptions, it is not a realistic rent-alone salary for most of London. Data as of April 2026 for tax assumptions and February 2026 for rents.

Is £40k Enough In London?

Often yes for a flatshare or a lower-cost setup in Outer London, but still tight for renting alone. At roughly £2,693 a month take-home, it is workable rather than luxurious.

Is £50k A Good Salary In London?

For many single people, yes. It is one of the points where London starts to feel more manageable, especially if you share housing or keep rent sensible.

Is £3,000 A Month Good In London?

It depends whether that is gross or take-home. As take-home pay, it is much more workable. As gross pay, it is nowhere near enough for most independent London renting.

Can You Live On £1,000 A Month In London?

Not realistically as an independent renter. Even average room rents in London were £985 a month including billsin Q4 2025, leaving almost nothing for transport, food, or anything else.

Is Buying In London A Different Salary Question?

Yes. Buying brings deposit size, mortgage affordability, service charges, and lender criteria into the picture, so it is a separate calculation from simply living in London as a renter.

Final Thoughts

Living in London is not one salary question. It is a housing question, a household question, and a take-home pay question.

For a single adult, the most useful test is not whether the headline salary sounds good. It is whether your likely take-home pay comfortably covers the living setup you actually want, with some room left for bills, savings, and ordinary setbacks.

If your offer only works with perfect budgeting, no rent increase, and no surprise costs, it is probably not a strong London salary yet. If it works with a realistic housing plan and still leaves some breathing room, that is a much better sign.

Jump to

Salary You Need To Live In London As A Flatsharer, Solo Renter, Or Family

Quick Answer By London Living Setup

Why The Number Changes So Much In London

The Benchmarks That Actually Matter

What Salary Feels Tight, Workable, Comfortable, And Strong In London

What Different Salary Levels Really Feel Like In London

Monthly Budget Examples That Make The Answer Easier To Judge

Renting Alone In London Is A Separate Question

What Is A Good Salary In London For A Family

Before You Accept A London Job Offer

Frequently Asked Questions

Final Thoughts

James Rowley

Author

James Rowley is a London-based writer and researcher covering London life, cultural geography, London travel, live London webcam pages and selected public figures across entertainment, sport, business and public life.

For over 15 years, he has focused on verified sources, first-hand local context and clear explanations that help readers understand both places and people more deeply. His work combines street-level London knowledge with careful research into career credits, media work, business interests and, where relevant, transparently explained net worth estimates.

He writes and reviews articles published on LondonWebcam.

Latest Articles

Popular Articles